Loan Management System

Seamlessly integrated, end-to-end solution designed for efficiency and ease.

What our Loan Management System can do?

CloudBankin lets you automate the entire loan lifecycle, steadying your top-line growth while building a solid customer base that will be delighted with your services! New products can be swiftly introduced, and tracking the repayment procedures is made much easier.

In addition, your decision-making becomes seamless and clear with features for generating module-wise reports. You can also adhere to processes and comply with audit requirements easily with a fully digital, cloud-integrated platform.

Easy to Use Dashboard

A single dashboard to manage a large client base gives you a one-stop tool for managing your products and clients.

Flexible Reporting

A host of analytical tools lets you view, export, and download a variety of customizable reports.

User-Friendly Workflows

Seamless, user-friendly workflows help process loan applications faster and more accurately.

Scalability

CloudBankin is designed to deliver exceptional performance and responsiveness to a greater extent, ensuring seamless loan management and enhanced customer satisfaction.

Security

CloudBankin offers peace of mind and security with state-of-the-art encryption features, VAPT testing, and cyber-security!

What Are the Key Features of a Loan Management System?

1) Loan Product Configuration & Setup

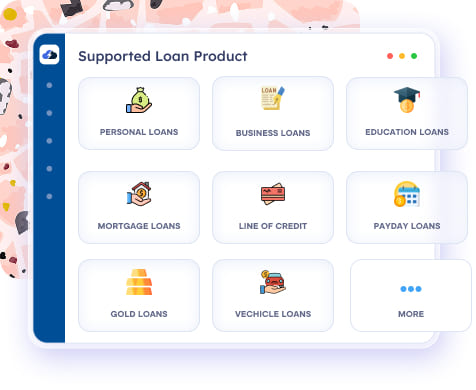

Supported Loan Products

Our LMS supports a wide range of loan products to meet diverse lending needs, including Personal Loans, BNPL, Education Loans, Payday Loans, Consumer Durable Loans, Line of Credit, Home Loans, Gold Loans, LAP, Auto Loans, and Business Loans.

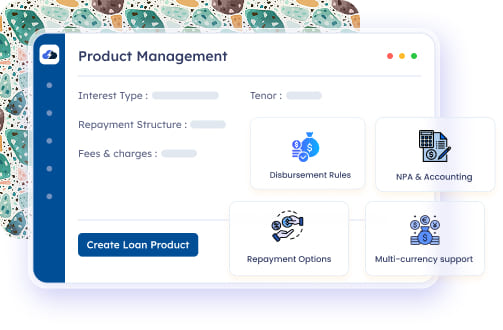

Product Management

Loan products can be created and configured to meet diverse lending needs, including secured and unsecured options, multiple variants, and multi-currency support. The system enables flexible interest types, repayment structures, and detailed product-level configurations to ensure operational efficiency and risk control.

Key capabilities include:

- Configure interest types (fixed, floating, declining, flat), amortization, and repayment structures (EMI, bullet, moratorium, variable installments, advance EMIs)

- Set tenure, repayment frequency, grace periods, arrears tolerance, and repayment strategies aligned with RBI norms

- Define fees, charges, penalties, GST, cash/accrual accounting, and memo accounting for NPA loans

- Configure disbursement rules (single, tranche-based, milestone-linked) and cooling periods

- Define collateral requirements, LTV rules, risk parameters, exposure limits, and product-specific approval workflows

- Enable or disable products by branch, channel, or partner, and configure co-lending products with partner-specific rules

This approach ensures products are fully configurable, compliant, and aligned with both operational and regulatory requirements.

Charges and Penalties

Configure and manage all loan-related charges and penalties with flexibility. The system ensures accurate calculations, automated taxation, and easy adjustments when needed.

Key functionalities cover

- Charges at product and loan levels: disbursement, installment, overdue, tranche disbursement, EMI bounce, processing, documentation, prepayment, and foreclosure

- Penalty calculation for overdue or delinquent loans using fixed, percentage, or slab-based rules

- Automatic application of GST and TDS on loan charges

- Support for charge waivers and reversals

GST & Tax Management

Automate tax calculations and ensure accurate financial posting across all loan products and charges:

- Configure GST by product, fee, and charge type

- Automatic calculation of CGST, SGST, IGST, and TDS

- Handle GST-inclusive and exclusive charges with posting to loan and accounting ledgers

Simplify reporting and compliance while maintaining data privacy:

- Generate invoices, debit notes, and credit notes

- Tax reporting, reconciliation, and audit trails

- Support refunds, waivers, and reversals

Mask sensitive tax identifiers such as GSTIN and PAN

2) Borrower & Loan Origination Data Management

Borrower Management

Our Loan Management System (LMS) delivers centralized Borrower Management as a single source of truth across the complete loan lifecycle.

Borrower data seamlessly migrates from LOS to LMS, supporting individual and business borrowers with unique borrower IDs across multiple loan products.

The system supports multiple borrower roles (primary borrower, co-borrower, guarantor), configurable application forms with multiple custom fields, and borrower segmentation by geography, risk, industry, or custom parameters.

It maintains historical borrower versions with effective date tracking, complete borrower history, audit trails, and masking of sensitive borrower information for compliance and security.

Document Management

Centralize all loan, borrower, and collateral documents in a single, secure repository with seamless migration from LOS via APIs. The system supports multiple document types, including KYC, income proofs, bank statements, business and collateral documents, agreements, e-sign, and Statements of Accounts, keeping all critical information organized and accessible.

Document requirements and checklists can be configured based on loan scheme, product type, borrower type, stage, and risk category. The platform handles both single and multi-tranche disbursals with stage-wise validation, duplicate collateral checks, and ensures proper linkage of documents to their respective loans and borrower accounts.

Complete document history is maintained for updates, replacements, and audits, while enabling reuse across multiple applications and accounts to improve operational efficiency. Automatic release of documents upon loan closure and generation of Statements of Accounts in required formats ensures accuracy, compliance, and smooth document workflows.

Collateral / Asset Management

Manage collateral end-to-end by linking assets to loan accounts and controlling the full lifecycle from capture to release:

- Collateral capture and linkage to loan accounts

- Valuation and revaluation scheduling (with legal approvals where required)

- Duplicate collateral checks and LTV ratio monitoring

- Collateral document verification and status tracking

- Partial and full collateral release handling

- Audit trails, access controls, and data security

Co-Lending Management

Set up and operate co-lending programs with flexible partner configuration and clear lender-level controls:

- Support RBI CLM-1 and CLM-2 models with configurable partner agreements, participation ratios, and exposure limits

- Lender-wise loan booking, ledgers, and income sharing

- Repayment, fee, and penalty allocation based on participation rules

Manage settlements and reporting with secure integrations and lender-level tracking:

- Escrow management, settlement, and reconciliation workflows

- Co-lender MIS, statements, and regulatory reports with API-based integration to partner systems

- Audit trails, access control, data segregation, and GST/tax handling for co-lender transactions

- Lender-level NPA classification and provisioning

3) End-to-End Loan Lifecycle Management

Loan Disbursement

Loan disbursement is executed seamlessly after loan approval and agreement completion, supporting both single-shot and multi-tranche releases with milestone-based scheduling. The system ensures accuracy, compliance, and transparency across all disbursement activities.

Key capabilities include:

- Validate disbursement amounts against sanctioned limits and verify borrower, vendor, or escrow accounts

- Support for co-lending fund splits, banking system integrations, APIs, and payment gateways

- Automatic calculation of disbursement charges and GST, with ledger postings

- Handle backdated/future-dated disbursements, cancellations, reversals, and re-initiations

- Real-time disbursement tracking, document and compliance checks, and full audit trails

- Automated notifications and secure file generation for bank processing

Repayment Management

Streamline repayments end-to-end with automated servicing actions like cancellations, reversals, restructuring, rescheduling, and penalty handling. The system supports multiple repayment frequencies (daily, weekly, fortnightly, monthly) across EMI and non-EMI structures.

Repayment schedules are system-generated at the borrower account level and automatically revised for tranche-based disbursements. It supports fixed EMI, reducing balance EMI, and bullet repayment, along with configurable repayment allocation strategies and moratorium setups (principal-only, interest-only, or both).

The platform supports prepayment, part payment, foreclosure, and excess payments, with interest computation on flat or floating (margin-based) rates, daily/monthly accrual, and flat-to-decline conversion. Collections can be processed via UPI, NACH, bank transfers, or cash, with full audit trails, backdated entries, bulk collections, and advanced options like interest waivers, RBI-aligned BPI calculation, amortization, fixed/variable installments, and interest-free periods.

NACH Management

Simplify repayment collections with fully automated NACH mandate processing, supporting both digital and physical formats:

- Create, register, and activate NACH mandates

- Auto-link mandates to loan accounts and EMI schedules

- Automate debit scheduling, retries, re-presentments, and bounce management with penalties and notifications

Manage mandate lifecycle efficiently while maintaining auditability and secure integration:

- Modify, pause, cancel, or handle expiry of mandates

- Auto-reconciliation via SFTP/API

- Integrated audit trails, accounting, and data security controls

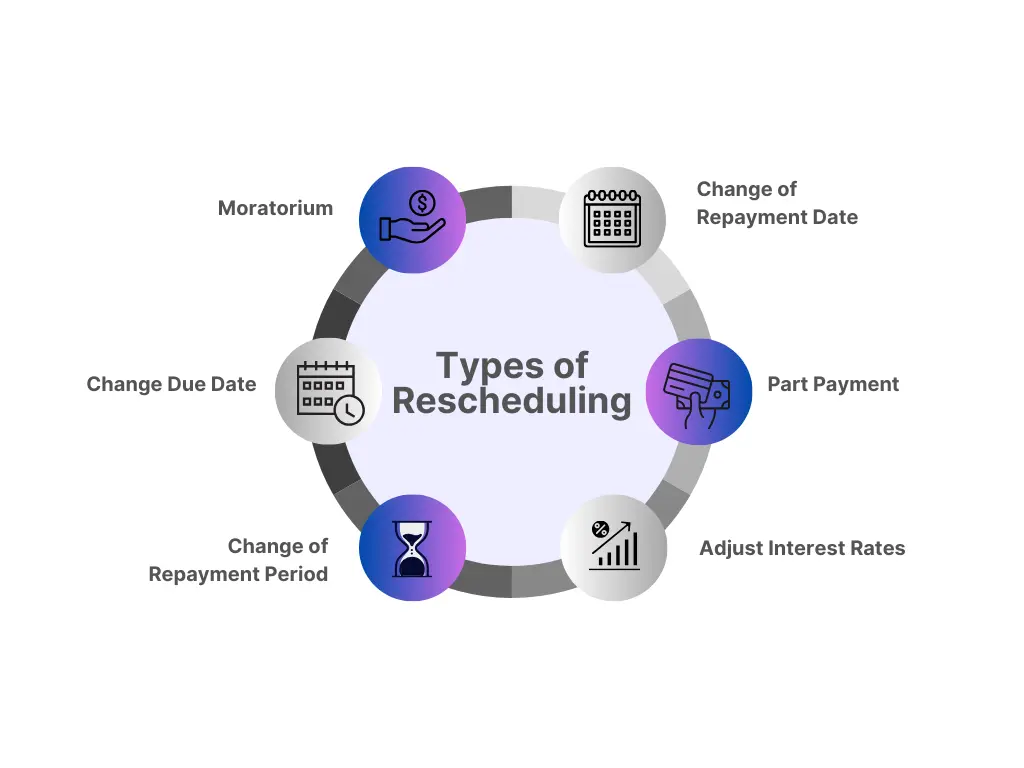

Loan Rescheduling

Easily adjust loan terms to accommodate borrower requests, policy updates, or regulatory requirements. The system ensures repayments remain accurate and aligned with agreements.

Includes:

- Extend repayment periods and adjust interest rates as needed

- Automatic EMI recalculation based on revised tenure and interest

- Rescheduling applicable to both principal and interest components

Foreclosure, Waiver, Write-Off, Part Payment & Prepayment

Manage full and partial loan closures, prepayments, and part payments with automatic adjustments to repayment schedules. The system ensures accurate recalculation of charges and interest based on loan product, tenure, or outstanding amounts, including refunds for any excess interest where applicable.

Waivers for interest, principal, penalties, or charges can be configured based on defined thresholds. The LMS supports both one-time and negotiated settlement workflows, automatically closing loan accounts upon completion and generating foreclosure statements and settlement letters for borrowers.

Automated notifications keep borrowers and lenders informed of all part payment, prepayment, foreclosure, waiver, and write-off events. Simulations can be performed before foreclosure or prepayment to assess impact, and bulk waive-offs help improve operational efficiency while maintaining complete audit trails for compliance.

4) Credit Risk, NPA & Regulatory Compliance Management

NPA Management

Manage delinquency and NPA workflows with structured classification, stage handling, and clear visibility into portfolio health:

- Automated DPD, SMA (SMA-0, SMA-1, SMA-2), and NPA classification as per RBI IRAC norms

- Interest suspense, stop-accrual, and reversal handling

- Provisioning by asset class, aging, and collateral

Control NPA movement and recovery actions with end-to-end tracking and reporting:

- NPA stage management (Sub-standard, Doubtful, Loss Assets) with upgrades, downgrades, restructuring, and write-offs

- Settlement and recovery tracking with automated accounting entries and audit-ready trails

- NPA dashboards, aging analysis, and regulatory reports with integration to collateral, recovery, and collection modules

Loan Provisioning

Automate provisioning by product, borrower type, and delinquency stage, including SMA/NPA-based calculations with collateral adjustments. The system supports partial, full, and co-lender provisioning and integrates with accounting to post automated journal entries.

Provisions can be reversed when accounts are upgraded, regularized, or settled, and calculations can be run daily, monthly, or on custom schedules. Provisioning dashboards and reports provides clear impact visibility on P&L and balance sheet, supported by audit trails for tracking and review.

Bureau Submission

Simplify credit bureau reporting by configuring multiple bureaus such as CIBIL, Equifax, Experian, and CRIF, with bureau-wise activation for seamless submissions.

The system maps submissions at product, borrower, and account levels to ensure accuracy, automates extraction of loan, borrower, and repayment data, and applies bureau-specific formatting for both individual and commercial accounts.

Submissions can be scheduled monthly, fortnightly, or on configurable cycles, ensuring timely and precise reporting.

Accounting

Automate and optimize all loan accounting processes with support for both accrual and cash-based methods, including interest and penal interest accrual. The system supports multi-branch and multi-entity setups with configurable product- and loan-level GL mapping, and handles both automated and manual journal entries, suspense accounting, and NPA provisioning. Key functionalities include,

- Generate loan ledgers, amortization reports, trial balances, P&L statements, balance sheets, and cash flow reports

- Manage accounts payable and receivable, invoicing, receipts, credit notes, and automated fee, GST, and TDS calculations

- Track overdue repayments, SMA account upgrades, penal interest, and generate demand reports with automated payment reminders

- Automate End-of-Day (EOD) operations, including interest accrual, fee posting, balance reconciliation, and reporting across all loan accounts

- Maintain audit-ready accounting trails for transparency and operational control

5) Lending Operations & Branch Management

Branch Management

Manage multi-branch and hierarchical structures with centralized control, ensuring each branch is configured for smooth loan operations:

- Branch master creation and configuration

- Branch-wise product, loan, user, and role mapping

- Loan origination, disbursement, servicing, and account management

Monitor branch performance and maintain accurate accounting while tracking operational metrics and reporting:

- Branch-level limits and exposure controls

- GL mapping and accounting integration

- Portfolio performance, PAR, and NPA tracking

- Branch-wise disbursement and repayment monitoring

- MIS, dashboards, regulatory, and audit reporting

- Configure branch holidays and working days

Bulk Action Management

Bulk actions simplify large-scale operations by enabling uploads and updates across offices, users, employees, serviceable areas, clients, loan accounts, and repayments. This reduces manual effort and ensures efficient handling of high-volume data.

Key capabilities include:

- Upload journal entries and chart of accounts using Excel/CSV templates or API integration

- Validate data with error reporting, partial success handling, and maker-checker approvals

- Secure, role-based bulk operations with complete audit trails

Notification

Keep borrowers informed and enhance operational efficiency with automated, event-driven alerts across the entire loan lifecycle:

- Automated Email and SMS notifications with configurable templates

- Event-based triggers for disbursement, repayment, overdue, bounced/failed payments, and loan closure

- Alerts for part payments, prepayments, foreclosures, waivers, and write-offs

Deliver messages across multiple channels while maintaining data privacy and customization:

- Multi-channel delivery: Email, SMS, WhatsApp (via integration), and in-app notifications

- Product-wise and branch-wise template configuration

- Consent management and masking of sensitive borrower data

- Automated alerts for SMA, NPA, collections, and other key loan events

6) Loan Analytics, Reporting & Security Framework

Reports and Dashboards

Access real-time operational dashboards and comprehensive loan portfolio overviews, covering active, closed, and delinquent loans. Analyze disbursement and repayment trends, collection performance, and key risk indicators, including DPD, NPA, SMA, delinquency ratios, Portfolio at Risk (PAR), Quick Mortality Rate, and Early Warning Signals, to make proactive and informed credit decisions.

The system supports branch-wise, product-wise, and loan-wise reporting, along with trial balances, balance sheets, and regulatory reports. Build custom and ad-hoc reports exportable in Excel, PDF, or CSV, and access MIS, management, board-level, audit, and exception reports for complete operational visibility and performance tracking across portfolios.

Security and Compliance

Control access and approvals across the platform with strong authentication and permissioning:

- Role-based access control with user-level permissions

- Maker-checker and approval workflows for critical operations

- Multi-factor authentication and secure login controls

- Password policies (expiry, complexity, lockout)

Protect data across storage, integrations, and file exchanges with security-by-design controls:

- Data encryption at rest and in transit

- Sensitive data masking (PAN, Aadhaar, bank and tax details)

- API security using OAuth 2.0 and token-based authentication

- Secure file transfers (SFTP) for banks, bureaus, and partners

Maintain security readiness across infrastructure, audits, and resilience planning:

- Comprehensive audit logs and user activity tracking

- Compliance reporting and audit-ready documentation

- VAPT certified with periodic vulnerability assessments

- SOC 2 compliant architecture and ISO 27001-aligned practices

- Cloud-agnostic deployment (AWS, Azure, on-premise) with cloud security controls

- Automated backups, retention policies, disaster recovery, business continuity

- Multi-entity and branch-level security segregation

What Are the Different Types of Loan Repayment Schedules?

Borrower Management

Key Highlights of CloudBankin's LMS

Why Choose The CloudBankin Loan Management Software?

Cost Effective

CloudBankin is an extensive, cost-effective, and fully customizable loan management system that can handle the ever-changing needs of your clients and a dynamically changing market.

Scalable

It suits multiple business lines. It is fully scalable, letting you grow your business with custom workflows and compliance tools for a variety of markets.

Reports

A fully digital, cloud-based platform helps lenders with accurate statements and reports for improved decision-making.

Secured and policy compliance

Auditing, tracking, and adherence to local regulatory standards is a breeze with a platform that is secured and built towards policy compliance for a variety of markets.

Frequently Asked Questions

What is CloudBankin Loan Management System (LMS)?

As your business expands, efficiently managing loan transactions can become increasingly complex. CloudBankin's Loan Management System simplifies this process, offering highly configurable modules for various loan types. It enables lenders to oversee customers across multiple locations through a unified platform, streamlining operations and enhancing decision-making. With CloudBankin, loan management is paperless, efficient, and scalable to meet the needs of growing businesses.

Can I use the Loan Management System to launch multiple loan products?

Our Loan Management System allows you to configure and launch loan products with customizable parameters, including principal and interest range, interest calculation methods, days configuration, broken period interest calculation, moratorium, NPA setup, charge configuration, and interest recalculation. It supports 12 loan types, including Personal Loans, Business Loans, Vehicle Loans, Gold Loans, Line of Credit, Payday Loans, Microloans, Agri loans, Loan Against Property, Microfinance, and Yearly Salary Loans, offering maximum flexibility to tailor products for diverse customer needs.

What type of Financial institutions can use Loan Management Software (LMS)?

CloudBankin’s Loan Management Software (LMS) is designed for diverse financial institutions, including Non-Banking Financial Companies (NBFCs), Fintech companies, Microfinance Institutions, Co-operative Banks, Credit Unions, and Banks, offering comprehensive, end-to-end lending infrastructure tailored to each sector's needs.

What is LOS and LMS in banking?

Loan Origination System (LOS) manages and automates the initial stages of the loan lifecycle, from application to loan disbursement. Conversely, a Loan Management System (LMS) handles the post-disbursement process, overseeing loan servicing, repayment tracking, and account management until the loan’s closure. Together, LOS and LMS streamline the complete lending journey for both institutions and borrowers.

Is accounting included in the LMS?

Yes, our Loan Management System (LMS) includes integrated accounting features with support for GST and TDS. It allows you to configure the Chart of Accounts (COA) for individual loan products, automatically generating journal entries for disbursements, repayments, and fees, while also permitting manual entries. Transaction data can be exported to accounting software like Zoho Books and Tally via API or bulk upload for efficient financial reporting.

How is the Collection & Repayments handled in the system?

Loan Management System (LMS) simplifies collections and repayments by supporting both auto-debit and manual payment methods. The system ensures timely repayments, updates loan balances, and amortizes principal and interest components for each payment. CloudBankin LMS also handles part-payments, loan foreclosures, rescheduling, charge and penalty waivers, and loan write-offs, providing comprehensive loan servicing capabilities.

How can a lender handle rescheduling of loans by using CloudBankin’s LMS?

Loan Management System (LMS) enables lenders to manage loan rescheduling and restructuring efficiently. The LMS offers four key functionalities: 1. Changing the repayment date, 2. Implementing a moratorium, 3. Extending the loan repayment period, and 4. Adjusting the interest rate for the remaining loan term. These flexible options allow lenders to customize loan terms to accommodate borrower needs, enhancing loan management and servicing capabilities.

Can we configure different charges inside the system?

Yes, we have the facility to configure different types of charges in our LMS with the below configurable parameters: 1. Charge Collection Time - at the time of disbursement, specifying due dates, instalment fees, overdue charges, foreclosure charges, etc. 2. Charge Calculation- flat amount, percentage of loan amount, percentage of interest, percentage of outstanding amount, percentage of principal partly paid, etc.

How is NPA management done in CloudBankin?

If a loan is overdue for certain days (for example, 90 days), as per RBI regulations, the loan will be marked as an NPA. Loan Management System (LMS) can track and generate a report of all the NPA cases. If all arrears are cleared, the loan will move out of NPA. We manage NPA in the following ways 1. Identify loans that are at risk of becoming non-performing. 2. Monitor their status regularly. 3. Send out an early warning in case a loan is going to be NPA. 4. Allow lenders to work with borrowers for repayment. 5. In case of a loan is not moved out of NPA, it can be written off or taken any other necessary action accordingly. Our LMS is there to make sure that it mitigates as many losses as possible for the lenders easily.

What's the rule engine?

Our rule engine is the credit decision-making platform that is configured with lenders’ credit rules & policies. It obtains data from various sources like PAN, Aadhar, Credit Bureaus, Bank Statements, SMS transactions, etc. It configures up to 2000 data points and can also integrate more based on lenders’ requirements. A lender gets the credit assessment memo as the output for their borrower’s eligibility.

Can I send emails via the system?

Yes, you can send emails via our system. This can be on the following ways: a) Event-based - You can send emails on events such as login, signup, non-repayment of borrowers, etc. b) Schedule-based - You can schedule to send emails with available email template formats on a daily, weekly or monthly basis. For reports, you must separately schedule to send emails to the given email IDs. Our system easily allows you to customize the templates used for sending emails. Email IDs and reports are configured in our database without any hassle.

Is template customisation possible in the LMS?

Yes, template customisation is possible in our LMS, which is useful for Sending personalised alerts & notifications for SMS and emails according to the availability of the variables. Generating loan agreements, loan closure letters, etc., as per the loan applications. This can be downloaded in PDF format under the respective loans.

Is reporting available in this system?

Yes, reporting is available in our LMS. There are 50+ reports, such as active loans, balance sheets, trial balances, general ledger reports, loan payments due, ageing detail, etc. By seeing the reports, lenders can get current snapshots of their businesses. The reports can be exported as CSV and can also be customized according to your requirements.

What are the Benefits of Having a Loan Management System (LMS)?

A Loan Management System (LMS) offers several benefits, including increased efficiency, enhanced accuracy, improved customer service, cost reduction, better regulatory compliance, enhanced risk management, and scalability. Transitioning to a paperless, agentless, contactless, and branchless model further simplifies processes and modernizes operations for financial institutions.

How to select a Loan Management System (LMS)?

Exploring these factors will guide you in making a well-informed choice when selecting a loan management system. Broader Coverage of Loan Types, User-Friendly Interface, Centralized Solution, Speed & Agility, Authenticated Access, Technology and Customer Service Support, Cloud Based or On-Premises Deployment, Better Third-Party Integration, Flexibility, Web And Mobile Compatibility, Data Security & Compliance, Scalability Cost.

What are the essential modules in the loan management system(LMS)?

The essential modules in the Loan Management System (LMS) are Reports & Dashboards, Audit Trail, Template Creation, Alerts & Notifications, Advance EMI, Top Up Loans, Rescheduling of Loans, NPA Management, Co-lending Module, Accounting, User Access Restrictions, Auto Write-off, Chart of Account, Recovery Repayment, etc.,

How long does it take to implement a loan management system?

The implementation of a loan management system typically takes about 2 weeks from onboarding, subject to various factors such as Data Migration, LMS setup, Third-party configurations, Accounting Configuration, and testing & matching repayment schedule.

How do I set up a loan management system(LMS)?

To set up a Loan Management System (LMS), begin with 1) Setting up your organizational structure. 2) Add Chart of Accounts. 3) Loan Product and Charge Setup. 4) Migrate data from the existing system. Then proceed with onboarding your customers and the loan servicing process.

How to Migrate From a Old System to a New Loan Management System?

The process of migrating from an existing system to a new loan management system involves any one of the methods below:1) Database - ETL (Extract, Transform, Load) 2) Through API 3) Bulk Import. And the process includes: 1) Understand the Database Schema of the Source System. 2) Identify the Modules Required for Migration. For example, Office, Clients, Loans, etc. 3) Decide the Migration Strategy, deciding whether to start from historical data or focus on data as of a specific date. 4) Write SQL queries tailored to extract relevant data from the source system efficiently. 5) Run Validations to ensure the output of SQL queries accuracy and adherence to predefined criteria, mitigating risks of data discrepancies during migration. 6) Create new loan products within the new Loan management system, configuring settings and parameters to align with organizational objectives and regulatory standards.

Can I generate collection reports for a specific period?

Yes, we can generate collection reports for a specific period. Our system offers over 50+ customizable reports, allowing you to generate reports tailored to your requirements.

Is API documentation available for LOS and LMS?

Yes, we provide comprehensive API documentation for both the Loan Origination System (LOS) and the Loan Management System (LMS) to facilitate integration with your existing systems.

What is the process for credit reporting to a credit bureau?

CloudBankin's platform automates the process of daily credit reporting to the bureau in the CIBIL format. This automation enhances accuracy and compliance while providing real-time insights into borrower creditworthiness, improving risk assessment and decision-making.

Related Articles

- Email: salesteam@cloudbankin.com

- Sales Enquiries: +91 9080996606

- HR Enquiries: +91 9080996576

After smartphone penetration, people are not watching their SMS at all. They use SMS only for OTP related transactions. That’s it.

But What can a Lender see in your SMS after you consent to them?

Lender can see income, expenses, and any other Fixed Obligation like (EMIs/Credit Card).

1) Income – Parameters like Average Salary Credited, Stable Monthly inflows like Rent

2) Expenses – Average monthly debit card transactions, UPI Transactions, Monthly ATM Withdrawal Amount etc

3) Fixed Obligations – Loan payments have been made for the past few months, Credit card transactions.

It also tells the Lender the adverse incidents like

1) Missed Loan payments

2) Cheque bounces

3) Missed Bill Payments like EB, LPG gas bills.

4) POS transaction declines due to insufficient funds.

A massive chunk of data is available in our SMS (more than 700 data points), which helps Lender to make a credit decision.

#lendtech #fintech #manispeaksmoney