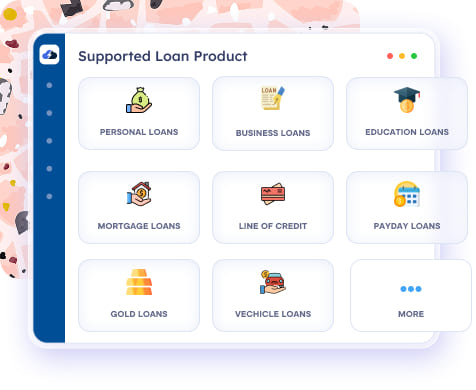

Streamline repayments end-to-end with automated servicing actions like cancellations, reversals, restructuring, rescheduling, and penalty handling. The system supports multiple repayment frequencies (daily, weekly, fortnightly, monthly) across EMI and non-EMI structures.

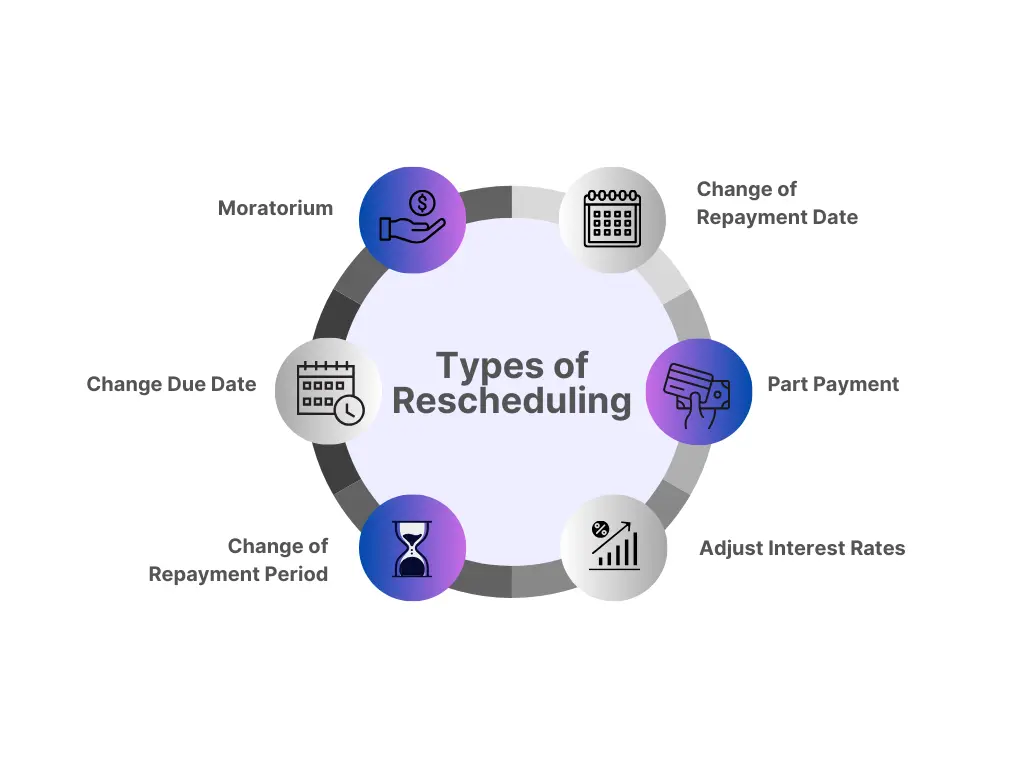

Repayment schedules are system-generated at the borrower account level and automatically revised for tranche-based disbursements. Maintain version-wise loan schedules with automatic principal and interest recalculation. It supports fixed EMI, reducing balance EMI, and bullet repayment, along with configurable repayment allocation strategies and moratorium setups (principal-only, interest-only, or both).

The platform supports prepayment, part payment, foreclosure, and automatic excess payments adjustment, with interest computation on flat or floating (margin-based) rates, daily/monthly accrual, and flat-to-decline conversion. Collections can be processed via UPI, NACH, bank transfers, or cash, with full audit trails, backdated entries, bulk collections, and advanced options like interest waivers, RBI-aligned BPI calculation, amortization, fixed/variable installments, and interest-free periods.

After smartphone penetration, people are not watching their SMS at all. They use SMS only for OTP related transactions. That’s it.

But What can a Lender see in your SMS after you consent to them?

Lender can see income, expenses, and any other Fixed Obligation like (EMIs/Credit Card).

1) Income – Parameters like Average Salary Credited, Stable Monthly inflows like Rent

2) Expenses – Average monthly debit card transactions, UPI Transactions, Monthly ATM Withdrawal Amount etc

3) Fixed Obligations – Loan payments have been made for the past few months, Credit card transactions.

It also tells the Lender the adverse incidents like

1) Missed Loan payments

2) Cheque bounces

3) Missed Bill Payments like EB, LPG gas bills.

4) POS transaction declines due to insufficient funds.

A massive chunk of data is available in our SMS (more than 700 data points), which helps Lender to make a credit decision.

#lendtech #fintech #manispeaksmoney